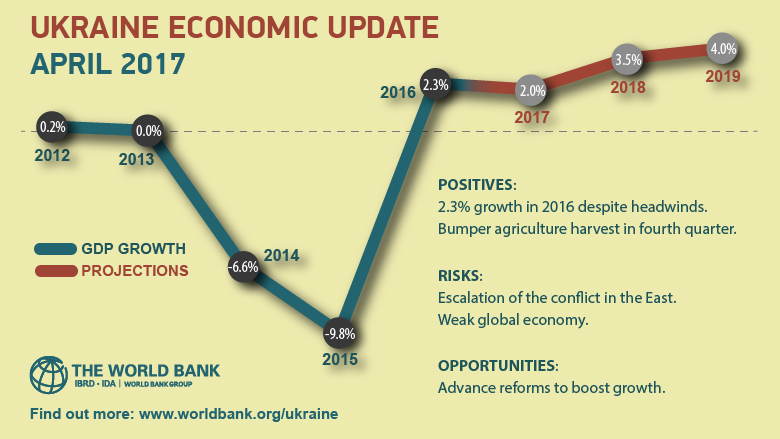

According to the World Bank’s latest estimates, Ukraine’s economy will grow by 2 percent in 2017. To boost annual growth to 4 percent in 2018-2019, however, Ukraine needs to overhaul the state pension system, land market and health care.

“The economy is recovering modestly, but accelerating reforms can help to boost growth in the medium term, address macroeconomic vulnerabilities, and improve the wellbeing of the population,” Satu Kahkonen, World Bank country director for Belarus, Moldova and Ukraine, was quoted as saying in the World Bank’s news release on April 4.

According to the World Bank’s economic update on Ukraine, the coal and trade blockade between war-torn Donbas and the rest of the country is expected to hurt two key sectors – steel production and electricity generation.

Ukraine’s government decided on March 15 to halt trade with the separatist-held territories until the separatists return Ukrainian companies they seized on March 1.

However, before Ukrainian authorities supported the blockade, initiated in January by veterans of Ukrainian volunteer battalions and political activists, Prime Minister Volodymyr Groysman said that the blockade will cause $3.5 billion losses for Ukraine’s mining and metallurgy industry.

The sharp increase in the minimum wage, installed in the 2017 state budget, will not help the state’s fiscal deficit, which widened to 2.2 percent of gross domestic product in 2016. Without a systematic fiscal consolidation, “Ukraine will need to rely on ad hoc revenue measures and expenditure cuts,” which would undermine debt sustainability, growth prospects, the bank’s report says.

According to the World Bank, Ukraine’s real GDP grew by 2.3 percent in 2016 after contracting by a cumulative 16 percent in the previous two years. Signs of a stronger growth of 4.8 percent emerged in the fourth quarter of 2016, if compared with the fourth quarter of 2015.

Inflation slowed to 12.4 percent in 2016 from 43.3 percent in late 2015, while real wages increased 11.6 percent in December 2016, if compared to December 2015. Labor market conditions remained weak, World Bank says, with unemployment increased to 9.3 percent in 2016 from 9.1 in 2015.

Stronger recovery has been held back by weak external demand, as well as Russia’s war against Ukraine.

“While a number of important reforms have advanced in recent months, a further acceleration in reforms is needed to boost investor confidence and bolster economic recovery,” the report says.

According to the report, reforms to increase private sector competitiveness, together with the real depreciation of recent years, should help support exports, while reforms to create fiscal space can unlock public investment, and reforms in the banking sector can permit a gradual resumption of lending.

The World Bank also notes that Ukraine will require significant external financing to meet repayments on the external debt of banks and corporates amounting about $7 billion per year during 2017-2019.

The International Monetary Fund approved another $1 billion loan tranche for Ukraine on April 3, bringing the amount lent to the nation to $8.38 billion. The IMF’s four-year lending program worth $17.5 billion started on March 11, 2015.

To get another $9 billion, Ukraine has to accelerate structural reforms, get rolling with privatization of the state enterprises, show results in fighting graft, and advance public administration reform.

The World Bank Group has provided a total of more than $4.4 billion to Ukraine since May 2014, including 4 development policy loans and 6 investment loans. The World Bank’s current investment project portfolio in Ukraine amounts to about $2.8 billion.